So, you just received a random check in the mail for $10,000 from your grandma Gertrude.

Or, maybe you're not so lucky, but you've been putting in the hard work and patience to save up an investing nest egg.

What do you do with it now?

More than likely, you've found this article because you have a lump sum burning a hole in your bank account, but you don't have a good plan for doubling it.

This is the ultimate guide to double your investment!

Within the spectrum of investing, there are always two factors that come into play: speed and risk.

Below, you will see some great strategies, some faster than others, and others for the more risk averse.

For example, if something has more speed stars, the faster it is for a multiplied ROI, and the more stars for a risk, the riskier it is!

So, if you're ready to find out how to best multiply your money, let's go!

*Disclaimer: no one here is a legal or financial professional, so do your own due diligence and seek out professional assistance before embarking on any financial investing.*

Chapter 1: Index Funder

How Following the Leader Can Make You Money!

Speed:

Risk:

Investing in index funds can provide a great ROI, which for the purpose of this article, could be used to double $10k.

We rated this as two (2) stars for speed, simply do to the amount of time it will take to 2x $10,000.

Plus, the risk is slightly higher than average due to nature of the entire market and system.

Here are the steps you can take if you wish to utilize this method.

5 Steps to Index Funding

Step 1. Check your accounts...

To start investing in index funds you first want to check your 401(k), IRA account, or Brokerage account.

A Brokerage account is an account that lets investors invest in the stock market. Investors can deposit funds and then buy investments.

To learn more about Brokerage Accounts look here.

To learn more about what the stock market is and how to invest in it look here.

Step 2. Pick your fund, not your nose...

Select which index you want to invest in.

Index funds can follow a particular asset, industry, or type of company.

Whatever fund(s) you decide to invest in, choose one that fits within your overall risk level and one that fits with your other (if any) investments.

To learn more about Brokerage Accounts look here.

To learn more about what the stock market is and how to invest in it look here.

Step 3. What's the minimums?

Check the minimum investment amount.

Don’t assume that index funds are all cheap, most have a minimum investment amount in order for you to buy in.

If you have less than the minimum amount you can go ahead and eliminate that as an option for the moment.

Step 4. Be part of the 1%

Look for funds that have an expense ratio under 1%.

Having the lowest possible expense rate will increase your time to achieving a return.

If you get stuck with a higher expense percentage, then it will be much longer for your investment to multiply.

Step 5. Fund and Auto-Fund

First, fund your account. Then, set your account up to have automatic contributions.

Here are a couple of good resources to read up further on the overall process and more details for investing in index funds.

Read about how to invest in index funds here, and investing in index funds explained here.

Chapter 2: Flip ~n~ Rent

Real Estate Tycoon Simulator IRL

Speed:

Risk:

If you find yourself binge watching HGTV, or think you could do what Chip and Jo do, this method is for you!

We gave a modest two (2) stars for speed and two and a half (2.5) for risk involved in this monopoly-style money maker.

Of course, it's not very likely that you alone could flip and rent a house for $10k, but this could be a great option for a group effort.

This is a good resource to help better understand this method, as well as this one.

1. Make a Plan

Have a plan and know your end goal. Your end goal should be based on realistic your financial capabilities, chosen investment strategy, and realistic expectations.

To learn more about goal setting for real estate, click here.

2. Your Network is Your Net Worth.

Connect with other local landlords/investors and get as much advice from them as you can.

Doing so can make a world of difference, something to keep in mind however is their investment bias. Investment bias is the landlord’s own purchasing strategy, experiences, and their own end goals.

This will help you find other investors/landlords who have similar goals but have much more resources than you do.

They can answer questions you may have and help further determine your investment strategy.

3. Down Payment Plan

Go to the bank and begin saving for down payment.

As soon as you start looking for a potential property start arranging your finances.

For the down payment you’ll want to have at least 20-30% of the price saved.

Also talk to your bank and find out how much you can afford to purchase.

4. Map Out Your Expenses

Do the math on expenses.

Every rental property has expenses, it’s important to know the potential monthly and unexpected expenses that a property will eventually have.

Here is a good resource to help.

5. Location, Location, Location.

Research and do your due diligence. Research until you think you can’t learn anymore then research some more.

When researching, look for several indicators of a strong real estate market (job growth, population growth, city revitalization, etc).

You will also need to do your due diligence when trying to find a strong real estate market. Adding the questions listed below to what is listed above will help you do that.

- Is the property located in a good school district?

- Are there businesses or attractions within walking distance?

- What is the property’s walk score?

- How many other rental properties are in the area?

- What does the crime rate look like?

- What is the average household income in the area or neighborhood?

- To learn more about doing due diligence in real estate, look here.

6. Inspect What You Expect

Get a home inspection.

Even though home inspections range in price from $250-$450 or more, they are absolutely worth the price.

The inspection can point out things that if left unnoticed or un-repaired can end up costing you quite a bit of money.

Also keep in mind that whatever the results are of the inspection can be used in the negotiation part of your real estate purchase.

7. Pro Forma

A pro forma in real estate is essentially a property’s cash flow projection.

These projections will help determine the property’s anticipated monthly cash flow, as well as expenses, including taxes and expected ROI.

8. Appraisal

Get an appraisal.

When planning on purchasing a rental property by financing, the lender will order an appraisal of the property.

This helps both parties know that they are paying the correct amount for a property and are not being overcharged.

9. Research Insurance Options

While it may seem obvious, it is important to not place unnecessary risk on your new investment property so make sure you get insurance.

Make sure to call around and speak with local agents to compare packages, prices, and coverage.

It is also beneficial to get an umbrella insurance policy as a landlord.

Umbrella insurance policies offer a second layer of protection in case of an unexpected accident or a lawsuit.

These policies will protect your property and also your other investment assets.

10. Make an Offer

When you find the a property you would like to invest in contact your real estate agent, if you’re using one, and they will fill out the paperwork and submit your offer.

Do not let your emotions take over, only spend what you can afford. Once you offer is accepted you are on the clock.

It’s wise to act quickly since the amount of time you have to close will vary.

It is also a good idea to move quickly and make sure the deal happens before the deadline.

If you have chosen to have a property manager, get started with the terms and agreements.

Your ROI rate all hinges on how quickly you can get the property rented out.

Chapter 3: Stocks

The Backbone of Wall Street

Speed:

Risk:

The New York Stock Exchange, NASDAQ, EuroNext, London Stock Exchange, TMX Group, Australian Securities Exchange, etc.

All of these things have one thing in common: stocks.

As one of the backbones of our current global economy, stocks are a pretty big deal.

We gave stocks a minimum of two (2) stars in both speed of return and risk, with a maximum of four (4) stars for both depending upon certain situations.

Let's dive in.

1. Assess Your Financial Situation

Before investing any money into stocks or bonds you need to ensure that your financial situation is in a position to accommodate it.

There are several things you should consider in order to determine this:

- Make sure your income and your job are both secure enough to allow you to invest.

- If you have any debt you probably need to focus on paying that down or paying that off before you even begin to invest. You should never invest money you can’t afford to lose.

- If you brought a baby into your family you may need all of your available income focused on helping that.

- You should have some extra room in your household budget that would allow you to put money into your investment(s).

It is also important to consider your goals and have an answer to the question of why you are investing in the first place:

- Are the investments for your retirement?

- Are the investments, instead, for a shorter term (5-6 year) goal?

- Will anyone else have access to the money?

2. Pick a Lane

Decide how you want to invest in stocks.

Are you wanting a more hands on approach or would you rather a more hands off approach?

Both are valid options, but for most the hands off approach would be recommended.

3. Open an Investing Account

In order to invest in stocks you need an investing account.

Depending on your level of involvement, that could be something like a brokerage account or opening an account through a robo-advisor.

Also, remember that 401(k)’s are a type of investment account as well so you may already be investing in mutual funds through that.

4. Set a Budget

When determining your budget, ask yourself two questions:

- How much money do I need to start investing in stocks? The amount of money you need depends on the price of the individual shares.

- How much money should I invest in stocks?

5. Invest Gradually

Invest in individual stocks gradually. Individual stocks should only make up about 10% of your entire investments.

Here's a good guide to help get into stocks, and here's another for how to invest in stocks.

Chapter 4: The Name is Bonds...

Standard Bonds

Speed:

Risk:

Bonds are another fundamental element in the global economy today.

Unlike stocks, bonds are a much safer because they are an investment that takes a lot longer to mature.

So, we gave bonds one (1) star for speed and a half (0.5) star for risk.

If you would like an additional resource, here is a good step by step article that will add to what is provided below.

1. Understand the Basics

Understand how bonds work.

When you buy bonds, you’re agreeing to lend your issuer a certain amount of money for a fixed amount of time.

In return, the issuer promises to make regular interest payments at a predetermined rate until the bond matures, at which your principal is repaid in full.

2. Open a Brokerage Account

You can purchase bonds through a brokerage firm which is in communication with governments and companies that want to issue debt.

Brokerage firms also have access to the secondary markets where bonds are sold.

3. Which Type of Bond?

Decide which type of bond you want to purchase. There are several different kinds of bonds to choose from:

")

4. Evaluate the Bond(s)

When investing in bonds it is important to evaluate them.

Evaluate the issuer of the bond since they will vary in reliability.

A majority of issuers will fall into these groups:

- The United States Treasury- considered to be the golden standard of reliability.

- Other United States Government Agencies- yield will be slightly higher than Treasury Bonds and risk is considered minimal.

- Municipal Governments- risk is slightly higher than federal government issued bonds.

- Foreign Governments- will carry either minimal or very high risk with corresponding low or high yields. This all depends on the nation offering the bonds.

- Corporations- Similar to foreign governments, the risk and yield of corporate bonds varies depending on the company issuing the bond.

5. Bond Grading

Another way to evaluate bonds is by looking at their grade.

Bonds are given a grade that indicates their credit quality and measures the bond issuer’s ability to repay the investment.

Bonds that are graded between AAA-C and AAA are the better bonds, with those closest to AAA being the best.

However, any bond graded BBB or higher is considered investment grade.

6. Bond Laddering

Invest in bonds with a laddered approach.

Bonds have differing maturing rates, therefore it is important to buy bonds with staggering maturing rates.

Remember, when you buy bonds, you're locking yourself into a given interest rate for a fixed period of time so it’s beneficial to have them mature at a staggered rate so you have more built in liquidity.

Want additional resources? Here is another article for investing in bonds, and here is one on how to buy bonds.

Bonus. Zero Coupon Bonds

Zero coupon bonds are different than standard bonds.

Zero coupon bonds are bonds that do not pay interest during the life of the bonds.

Instead, investors buy zero coupon bonds at a deep discount from their face value, which is the amount the investor will receive when the bond "matures" or comes due.

If you're interested in finding out more, check out this article.

Chapter 5: Margin Trading

Borrowed Money Making Money

Speed:

Risk:

Margin is the money that is borrowed in order to invest.

Here's everything you would need to know about margins.

This is why it is highly risky, but also potentially rewarding because you're technically using someone else's money to make money.

The opportunity to double any investment that you partner with a loan, is exponentially increased with this method.

There are some requirements for margin trading to make sure you are aware of prior to starting.

1. Open Up a Margin Account

A margin account is an account opened specifically with a broker to be able to start margin trading.

They are generally subject to minimal account balances that are often based on the loan-to-value ratio of the account.

Here is a great guide to opening a cash or margin account.

2. Buy

Buy stocks with borrowed funds.

The whole point of margin trading is to buy stocks with borrowed funds.

By using borrowed funds to purchase stocks, the profits gained can be greatly increased compared to spot trading.

Check out these good strategies!

3. Hold

Hold for a short period of time.

Consider setting one or two month windows for margin purchases so that you are not exposed for too long to unforeseen price drops or market corrections.

Here are some general principles for margin trading.

4. Sell

Sell when the stock reaches a predetermined benchmark.

Don’t get greedy, set a target price up front that you are hoping to reach.

If the price exceeds your target, reevaluate and consider selling.

Here is a guide for day trading on the margin.

Chapter 6: Land Flipping

Dirt Never Looked So Good

Speed:

Risk:

House flipping is the way that most people believe you could make incredible ROI in real estate, but that's because people often forget about the land.

Without the large expenses of renovating and updating a home, flipping land can provide an equally exciting return.

We rated the speed to achieve a double investment at three (3) stars, and the risk potential is on average higher as with any large asset acquisition.

However, with these proper steps, you can reduce the risk and achieve your investing goals faster.

1. Market Research

When starting to invest in land it’s wise to look into several markets.

Most markets will have plenty of opportunities, however the type of properties and the price range both vary throughout.

Here are some other tips for market research:

- As much as you can, define what your ideal property looks like

- Establish your budget both for marketing and for buying property.

- Identify the state and local laws that apply to vacant land transactions.

- Decide whether you want to sell for cash, with seller finance, or both.

2. Direct Mail Marketing

Direct mail marketing is considered to be the most efficient and cost-effective way to find motivated sellers.

The success or failure of a direct mail marketing is all dependent upon your ability to find and organize the right data and to send compelling messages to the right people.

Determine if you are going to get your list of property owners from the county or a data service.

For the best response rate, get your list filtered and sorted.

To ease the process of mailing your offers out, you can try using a direct mail service provider (such as Vistaprint, Mail Shark, or Every Door Direct Mailer).

3. Process Leads and Make Offers

Make sure you have the right systems in place to manage the responses you get from your direct mail campaign.

Set up a phone system, with a custom voicemail recording, to answer the sellers who choose to call you.

Create a buying website that gives potential sellers a way to submit their property information to you online.

When responding to leads, gather the essential information you’ll need to close.

Set up a system for noncommittal offers.

A way to do this is to send blind offers along with your Direct mail marketing.

If you have to negotiate, only do so on the properties that are worth the fight and always make sure the price fits within the amount you are willing to pay.

4. Proper Due Diligence

Once you offers start getting accepted, you need to start doing your due diligence.

In order to feel confident about your investment, you need to do your own research.

Find out all the information about the property that you can and verify that it is all correct.

Figure out an approximate market value of your property by looking at looking at similar properties listed in the vicinity.

Here are 19 tips for due diligence when buying land from some real estate pros.

5. Close on the Acquisition

There are two main ways to close, one is with a title company/real estate attorney, or you can close it yourself.

For properties under $5k- Do your own title search to verify a clear chain of title and conduct an in-house cash closing.

For properties over $10k- Send your signed purchase agreement to a professional closing agent and let them do all the work.

For properties between $5k-$10k- Take the hybrid approach, by ordering title insurance and closing the transaction yourself.

Check out this good read on how to close on a land contract.

6. Make it Shine

Most properties will need some work to look better.

Depending on the property, it could be as simple as raking the leaves.

Others may require land clearing such as removing a stump, clearing out some weeds or ugly plants, or putting visible markers where a potential driveway may go.

The goal is to make prospective buyers see the potential in your property.

7. List, Sell, and Promote

Now that you have a property or properties, what do you do now? Sell them of course!

Properties sell at different speeds, some will sell much faster than others.

How quickly the sale happens has a lot to do with the quality of the listing and how desirable the geographic area of the property is.

Start by creating a compelling property listing.

Things to include are having great pictures, an informative description, and even a video if possible.

Post your property listing in as many places as possible.

Focus your efforts on locations with the highest traffic and/or the most targeted audience.

Price your property competitively.

It also helps to offer seller financing whenever possible.

Check out this great resource to help.

8. Process Buyer Leads

When you post listings on the internet, you’ll have a lot of people responding to them.

Many of the people won’t be serious about buying but they feel compelled to ask questions.

Follow up with every single email, text, call, and comment on your listing.

It’s normally not possible to know if someone is a serious contact on first contact, so it’s incredibly important to follow up with everyone.

9. Close the Sale

The closing process can vary in complexity with the buyer, the property, the state laws in effect and whether the property is being sold for cash or on terms.

When you have an interested buyer and you have get them verbally committed, you need to schedule a closing date.

Depending on what the profit margin is in the deal, it might make sense to get a title company to handle the paperwork and the closing.

However, if the profit margin is smaller, the closing can happen in-house.

Simply sign over the deed to the buyer once you have been paid.

If you're wondering about the lifecycle of the land flipping process, check this out.

Bonus: Seller Financing

While you don’t have to offer seller finance, if you do you can expect your properties to sell faster, sell at a higher price, while also generating some passive income.

Offering seller finance will also make a lot more money in the long term.

Read up on these pros and cons of owner financing for more info.

Chapter 7: Home Renovation

The Long, Long Game

Speed:

Risk:

If you own your home, and one day plan on selling it, then there is no greater way to increase your potential ROI than by simply upgrading / renovating.

This investment could potentially increase your selling price significantly, or it could simply boost your morale while you live there.

Since selling is potentially far down the road, we rated this method one (1) star for speed and a half (0.5) star for risk.

Improvements that give the Best ROI

In reality, your home may be your largest investment.

If parts of your home is outdated or any of it needs to be renovated or repaired some of those improvements may have a direct impact on the value of your home.

A list of improvements that will improve the value of your home are listed below:

- Put new siding on your house.

- Put a new roof on your house.

- Replace the windows on your house.

- Improve small parts of your kitchen or bathroom, like replacing the countertops with granite ones.

Remember, you don't have to make large investments to see a major improvement in value.

Chapter 8: Online Savings Account

ROI in a Lifetime

Speed:

Risk:

This is the most basic method available, to the point that if not for the better interest rates of online accounts, there wouldn't be an ROI.

Simply because the speed would suggest that this isn't an investment.

We rated this with zero (0) stars for speed because it takes so long to get a double ROI.

However, we gave it zero (0) stars for risk because this is one of the absolute safest methods of investing.

2-Step Savings Method

- Research your options. Online savings accounts can have better interest rates than your local bank (Here are some current rates.) Make sure the FDIC insures the bank. Make sure you read the fine print about withdrawals, the last thing you need is to not have access to your money when you need it.

- Start adding money to the account you choose.

Chapter 9: Invest in a CD

Singing Not Required

Speed:

Risk:

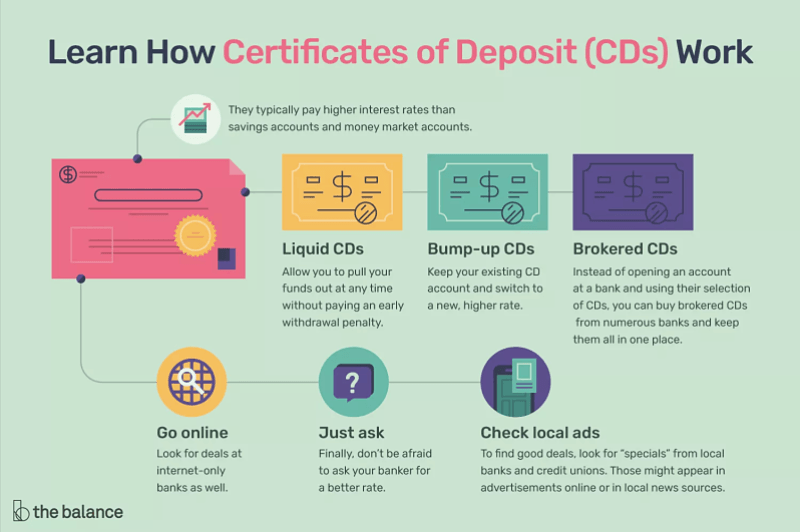

A CD, certificate of deposit, is one of the safest investments on the market today.

With a set amount of time, your investment gains a small percentage growth over the maturation of the investment.

We rated this with one (1) star for both speed to ROI and risk, simply because of a technique suggested below.

1. Find the Right Institution

The FDIC and the NCUA insure banks and credit unions, respectively.

If you have a CD at an insured institution you will be protected by insurance to the maximum allowed by law.

Here are 9 tips for choosing a CD account.

2. Pick the Right Term

When opening a CD one of the first things you need to decide is how long you want to have your money tied up.

The longer the term length, the higher interest rate you’ll earn.

3. Choose Your Type

There are several different types of CD’s, they are not one-size-fits-all. Find out which one works best for you. Below is a list of some of the options:

- Traditional CD- You receive a fixed interest rate over a specific period of time. When that term ends, you can withdraw your money or roll it into another CD. Withdrawing before maturity can result in a hefty penalty.

- Bump Up CD- This kind of account allows you to swap your CD’s interest rate for a higher one if rates on new CDs of similar duration rise during your investment period. Most institutions that offer this type of CD let you bump up once during the term of your CD and keep the interest rate for the remainder of the original CDs term.

- Liquid CD- This kind of account allows you to withdraw part of your deposit without paying a penalty. The interest rate on this CD usually is a little lower than others, but the rate is still higher than the rate in a money market account.

- Zero-coupon CD- This kind of CD does not pay out annual interest, and instead re-invests the payments so you earn interest on a higher total deposit. The interest rate offered is slightly higher than other CDs, but you’ll owe taxes on the re-invested interest.

- Callable CD- A bank that issues this kind of CD can recall it after a set period, returning your deposit plus any interest owed. Banks do this when interest rates fall significantly below the rate initially offered. To make this type of CD attractive, banks typically pay a higher interest rate. These accounts are typically offered through brokerages.

- Brokered CD- This term refers to any CD offered by a brokerage. Brokerages have access to thousands of banks’ CD offerings, including online banks. Brokered CDs will generally carry a higher rate of interest from online and smaller banks because they’re competing nationally for depositors’ dollars. However, you’ll pay a fee to purchase the account.

4. Review Rates

Once you’ve decided what type and what duration you want for your CD, you need to find out what rates are available at different banks.

Here are the places with the best CD rates for 2020.

5. Options for Collecting Payments

Decide when to collect your interest payments.

You have options when it comes to collecting your interest payments.

You may be able to receive your interest payments monthly or once a year.

Once the term of your CD ends, you will receive your initial investment back and also your last interest payment.

6. Consider Laddering

While CD investment has its drawbacks, one way to reduce those is to use a technique called laddering.

Laddering is a strategy that gives you regular access to your cash and protects you against rising interest rates.

Laddering is much more simple than you think.

Instead of investing all your money as one large sum in a single CD you divide your money into equal parts and invest each in CDs of varying terms.

Laddering gives you a couple benefits:

- Penalty-free access to your money each time a CD matures.

- Access to more favorable interest rates since a portion of your investment will be invested into a long term CD.

- Access to better returns if interest rates are higher when you re-invest.

7. Fund the CD

Choose the best funding method / source that works for you.

Options include online transfer, phone transfer, or mailing a check.

Chapter 10: Peer-to-Peer Lending

Lending Money Made Easy

Speed:

Risk:

P2P lending is a great way to both boost capital and gain a great ROI...

If you partner with the right organizations.

We rated the speed of potential return at three (3) stars, and the risk a variable three and a half (3.5) stars.

1. Open a P2P Account

Open an account with a P2P lender and put money in the account.

Select a platform and register on it.

You will need to fill out basic information and create a login ID.

You’ll also need to provide self-attested copies of PAN and address proof for verification.

You will create an investor account to start a financial transaction and you may be asked to pay a one-time non-refundable registration fee at the time of signing up.

2. Interest Rate

Set the interest rate you’d like to receive or agree to a rate that’s on offer.

Interest rates vary based on the borrower’s ability to pay and their credit score.

Set a rate you would like to receive or find one that fits your comfort level.

What's the difference between Per-to-per loan vs. Bank Loans?

3. Proposal

You can start by sending your proposal to borrowers.

An investor can commit to lend money to a single or multiple borrowers.

4. Verify Credentials

When a commitment has been made the borrower will have to be verified further.

This helps ensure that the borrower isn’t likely to default on their payments.

Once verified the loaner and the borrower sign a loan agreement.

Some P2P lending websites allow you to view the borrower’s documents by paying a viewing fee.

5. Dispersal

Loan dispersal begins once the loan agreement has been signed.

Both the dispersal and loan repayment are done in an escrow account.

The lender has to fund the account with the amount they wish to invest beforehand.

Chapter 11: Mutual Funds

How to Make Money with All Your Friends

Speed:

Risk:

Mutual Fund investing is one of the best ways to invest if you are just starting out.

We rated the speed of potential return at one (1) star, and the risk a variable (1) to (2).

Continue reading for our step by step guide for mutual fund investing.

1. Go with the grain or against it

Decide if you want an actively or passively managed mutual fund.

When trying to decide you should try and answer this question: do you want to try and beat the market or mimic it?

2. Calculate Your Budget

Remember that a good rule to follow is that you should feel comfortable leaving the money untouched for at least 5 years.

Here are a couple further questions to help you figure out how to calculate your budget:

- How much do I need to get started? Mutual fund providers often require a minimum amount to open an account to begin investing. Brokers, on the other hand, may have no account minimum, while others can range from $500 to $3,000.

- How should I invest that money? What mix of funds is right for you? Age plays a large factor in this decision. The closer you are to retiring, the more you’re looking for investments that prioritize the preservation of capital over returns. Younger investors have more time to ride out their investments so they can choose more risky investments.

Here is a good tool to help calculate your mutual fund expense ratios.

3. Research Fun for the Mutual Fund

Just like when investing in stocks, you need a brokerage account and with mutual funds you do have some options.

If you have a 4019(k) there’s a good chance you are already investing in mutual funds.

Another option is to buy the funds directly from the company that created them, such as Vanguard or BlackRock Funds.

Many investors choose this 3rd option, and that is buying from an online brokerage.

The benefit of buying from an online brokerage is that they offer a broad selection of mutual funds across a range of fund companies.

If you go with an online brokerage, you will want to consider these things:

- Affordability- Mutual fund investors can face two kinds of fees: from their brokerage account and from the funds themselves.

- Fund choices- Retirement plans from employers may only offer a dozen or so mutual funds. You, realistically, want more options than that. Brokers, on the other hand, offer hundreds to thousands of no-transaction-fee funds to choose from.

- Research and educational tools- The need for researching and thinking increases with the amount of choices that are available with using an online brokerage for your mutual funds. It’s important to pick a broker that helps you learn more about a fund before investing your money.

- Ease of Use- You need to be able to understand a brokerage’s website or else it won’t be helpful. You want to feel comfortable with the experience.

4. Minimize Your Fees

It always pays to minimize costs and fees associated with funds because they can eat into your returns over time if you don’t.

Generally, you are looking for expense ratios that are below 1%.

5. Pick a Diversified Portfolio

It’s important to own funds in different investments.

If you own 5 different funds but they are all of the same investment, there is no diversification.

It’s simply like you owning one larger fund.

You want to have funds in investments such as stocks, bonds, real estate, etc. another way to keep your portfolio diversified is to rebalance your portfolio once a year.

For example, if one part of your investments had great gains and now constitutes a bigger share of the pie, you might consider selling off some of the gains and investing in another part to regain the balance it once had.

6. Find a Family of Funds

Find a company that offers a family of funds that work for you.

The least expensive way to set up accounts is directly with the fund company that offers shares.

If you can find a company that offers a family of funds, then it makes things much easier for you.

7. Invest and Monitor

Invest in a fund.

Then continue to monitor the fund to ensure balance.

Once you have picked a fund and invested in it your job is not over.

You need to continue to monitor your funds to make sure everything is running smoothly.

Remember, past performance is not a guarantee for future performance.

Chapter 12: Domain Flipping

Big Names Make Big Bucks

Speed:

Risk:

Domain flipping is a potentially lucrative investment, if you know how to get a return.

By finding the right site with the right potential, you can turn a small investment into a very tidy profit.

We rated this method with two and a half (2.5) stars for speed to return and two (2) stars for risk.

With the right plan, and a bit of luck, you could find yourself on the fast track to a maximum ROI with minimal risk.

1. Getting Started

First, know your budget.

Like every other investment, you must first know your budget.

It is always best to start off by investing a small amount of money and then move on to making a bigger investment once you feel comfortable.

Second, choose a niche.

Selecting a profitable niche is very important when it comes to domain flipping.

Having adequate knowledge in searching domain names is critical.

Carving out a niche will help you be able to seek out potential buyers actively who would be interested in what you are offering.

")

2. Calculate Value

Determining the value of a given domain name is the most important skill you can learn in domain name flipping.

There are several tools available to improve this skill:

- Namebio has a database of more than 500,000 historical domain sales. They have filter features which can help you narrow down the domains by several different categories. Sifting through the listings long enough will develop your instincts.

- There is an app named The Domain Game available for IOS and Android where they give you a domain and you have to guess whether it sold for three, four, five or six figures. You get points for answering correctly and lose them for being wrong. Do this long enough and your mind would start connecting the dots.

3. Hot Keywords

Before buying domain names you should make sure that you are focusing on finding keywords that buyers would be interested in.

A clue to look for is picking a domain name with acceptable traffic, which would have around 10,000 searches a month.

Using tools such as Google Keyword Planner and niche finder software can help you do this.

A general guide for looking for keywords may also help:

- Generic names are a great find because they can be used to describe new and upcoming products and services, however you must also look into copyright and trademark issues beforehand.

- Business names combined with geographic names like chiropractor Los Angeles can be sold conveniently.

- Timely names pertaining to major events like Wimbledon and the Olympics have great potential to become best sellers.

- Geographic names related to countries and cities can be sold to web developers looking to start new communities, businesses or portals.

4. Due Diligence

- Check backlink profile- Backlinks are any public website that “links” to the domain in question.

- Check email spam databases- Check the domain in a database like UltraTools to see if it’s on any blacklists. There are ways to dispute blacklist placements, but it may not be worth all the time and energy.

- Review Web Archive’s versions of the website- Examine the website’s history. This is very useful for several different reasons. It could help you identify a potential buyer by analyzing the content of the website. It can also signal red flags if the domain was being used for something shady.

- Check DA/PA- A domain’s “Domain Authority” and “Page Authority” seem to identify a domain’s ability to rank in the search engines. This means that a domain with a higher DA/PA will usually have a higher value. This is not the only indicator if a domain will sell high, it is just one factor.

5. Finding Domain Names

- Focus on local domain names- Search places like GoDaddy and Namecheap for the domains that local businesses would be interested in.

- Find an existing domain name- Using Sedo you can find existing domains with a potential for profit. Make sure you pick domain names that have good traffic. Make sure they have good backlinks and Google PageRank under 17 characters as well. However, when searching for domains, steer clear of existing domain names containing special characters or numbers because they are much less likely to be sold.

- Find domains related to your keywords- Using Namecheap to search for domains using relevant keywords has become increasingly popular.

- Don't limit your search to domain names with “.com”, “.org”,or “.net”. Broaden your search to include domain names with “.us” and “.io” just make sure you do your due diligence with each of them.

6a. Buying New & Current Domain Names

- Buy a new domain- Although most generic domain names are usually taken, you could be lucky enough to find an unregistered one. If you happen to find an unregistered domain name, don’t waste a second. Register it with the best domain registrar company you can find because that will allow you to sell your domain to the interested party easily.

- Buy domains with page rank- Even though domain names that were previously used by other businesses are usually about to expire, they are still worth a lot of money if they have a good number of backlinks and a ranking of five or more.

6b. Buying Expired Domain Names

In order to retain ownership of a domain, you must renew it annually, if you don’t it “expires”.

Expired domains go through several stages before being released, and the process varies between registrars.

Expired domains are potentially more valuable than new domains because expired domains have history.

Age, traffic and SEO properties like domain DA/PA give the expired domain it’s potential value.

All of that seems great but expired domain names must carefully be vetted and scrutinized thoroughly.

These domains have been used before and you have no idea what their history is.

The expired domain you are looking at could have been blacklisted in search engines, it could have been used for spamming or illegal purposes, it could have been used to defraud monetization networks like adsense or many other things.

This is why it is so important to do your due diligence.

The most popular place to find expired domains is ExpiredDomains.net.

7. Build Up a Portfolio

Building a solid domain portfolio is not easy, it could very well take you months or even years to achieve this goal but it is definitely worth it.

8. Mix Up Your Sales Strategies

- Set a Price- You can set a particular price for domain names you have to offer when you are not in a rush to sell them. If you have a large portfolio this strategy is usually what you will adopt.

- Auction- Sell your domain to the highest bidder. Sites like. GoDaddy and Namecheap follow the auction strategy.

- Make an Offer- When you have a niche domain, you can find prospective buyers and make offers if they are interested in buying.

9. Never Sell Immediately

Domain flipping is not always about making quick cash, think of domain flipping as more of an investment.

In reality, you may have to spend days in research before you make a profitable sale, and the general rule is that it is better to wait for several months or years in order to sell a domain name for a greater profit than to rush and have to settle for normal profit.

Chapter 13: Rank and Rent Little Websites

Local Lead Generation Machine!

Speed:

Risk:

IMO this is the absolute greatest method for doubling $10k quickly!

So much so that we've given it four and a half (4.5) stars for speed to ROI, and two and a half (2.5) stars for risk.

The value of this investment method is no joke at all.

In 2015, I was like many reading this...

Stuck in a meaningless 9-5, looking for ways to increase my income on the side.

Then, one day I quit...

After I had found this.

I have been self-employed ever since, building little websites like these and renting them out to local business owners:

This little tree service site makes me about $2000 per month.

Why?

Because it generates about 250 calls for my client.

In fact, it's been making me $2k every month since 2015!

This is why I believe that this is the best possible method for doubling your $10k investment.

Apart from the time to do the research, build, and rank the website... The costs are minimal.

Plus, the two things that really make this method succeed aren't going away anytime soon:

Small Businesses and the Internet.

When you know how to produce leads, then you can get paid directly from local businesses.

We have a coaching program with over 5000 students learning this business and creating real income online by providing a real service.

Go to this page to find out more about how you can maximize your investments with this method.